Few things are as disappointing as a lost sales opportunity. The time spent nurturing leads and presenting solutions feels wasted when a potential client chooses a competitor or decides not to buy. Lost sales opportunities impact revenue, market share, and team morale.

However, they also offer valuable learning opportunities. In this blog, you’ll learn how to analyze the root causes of each lost sales opportunity and implement strategies to minimize future losses. You’ll also learn how to calculate lost sales opportunities.

Let’s get started.

What is a lost sales opportunity?

A lost sales opportunity occurs when a business loses a potential deal due to various factors that prevent the completion of a transaction. For example, whenever a lead already in your sales pipeline decides not to make a purchase, you’ve lost a sales opportunity.

This can happen for many different reasons—let’s look at some of the most common ones.

Possible reasons for a lost sales opportunity

Weak customer service

If your customer service game is poor, you’ll rack up missed opportunities. A potential customer is more likely to refuse to complete a purchase if they are faced with deterring issues like:

- Long response times.

- Inadequate product knowledge.

- Unresolved problems.

- Unprofessional staff.

- Limited support channels.

Inaccurate demand forecasting

Sometimes, you may simply have missed the mark in predicting customer demand. That can translate into stockouts, meaning you can’t complete a sale even when the customer is willing and ready to buy—in other words, a lost sales opportunity.

Supply chain disruptions

An optimized and stable supply chain is crucial to maintaining steady sales cycles. Breakdowns in that chain often result in delayed production schedules and an inability to meet customer demands promptly.

Suboptimal inventory management

Sometimes, businesses undermine their selling chances with poor inventory management. Seemingly minor issues like improper labeling and store management can lead to avoidable delays and, ultimately, a low level of customer satisfaction.

Pricing strategy missteps

Setting the right price is crucial to every sales strategy. Your product’s or service’s pricing must align with prevalent market rates. Otherwise, customers will gladly seek out your competition.

Insufficient marketing

Insufficient marketing is another common reason for losing sales opportunities. With poor marketing comes poor brand exposure and low customer engagement, ultimately leaving your sales team with a significant hurdle to overcome.

Misalignment with customer needs

Customers make purchasing decisions based on their needs. If your product or service offerings do not fit their budgets or meet their expectations, requirements, or pain points, you are bound to lose sales opportunities. Sometimes, alignment is about getting your timing right to offer potential buyers a good deal when they’re desperately searching for one.

Competitor outperformance

In some instances, you have to admit that an industry competitor is doing a better job of meeting your potential clients’ needs. You can’t be everything for everyone—but in these cases, it’s smart to take a few cues from them to up your own game.

How to measure the cost of a lost sales opportunity

The cost of lost sales opportunities represents the potential revenue and profits forfeited when a sales opportunity is missed. Accurately measuring this cost can help you:

- Evaluate sales performance.

- Identify areas for improvement.

- Optimize sales strategies.

Here are the metrics you need to track in order to calculate your lost sales:

- USP = Unit selling price.

- FAD = Forecasted annual demand.

- SF = Shortage factor (percentage of demand that couldn’t be met).

- UFR = Unit fill rate (percentage of demand that was met).

Once you have those ready, the formula looks like this:

Cost of Lost Sales = USP * FAD * SF * (1 – UFR)

Multiply the unit selling price (USP) by the forecasted annual demand (FAD) to determine total potential revenue. Multiply the result by the shortage factor (SF) to calculate lost sales revenue. Then, multiply by (1 – UFR) to account for potential upsell/cross-sell revenue lost.

For example, if the unit price is $5.00, demand for the product is 700 units, the fill rate is 90%, and the shortfall is 20%, then the item’s lost cost of sales is calculated as follows:

LSC = 700 units/year x $5.00/unit x 0.2 x (1 – 0.9) = $70/year

7 ways to prevent lost sales opportunities

1. Automate lead generation and nurture

According to our research, 80% of marketers using automation software manage to generate more leads. You’re more likely to let sales opportunities slip through your fingers with manual lead generation and nurturing processes—they are simply cumbersome and time-consuming.

With automation, it’s easier to capture, track, and nurture your leads with custom messages in a fraction of the time. Plus, there’s the added advantage of being able to take on more leads.

2. Stay on top of your inventory

If you get your inventory game right, you’ll:

- Forecast demand more accurately.

- Minimize stock-outs.

- Improve delivery timelines.

Ultimately, you’ll satisfy your customer base more often and never miss a sales opportunity again.

3. Diversify your suppliers

This involves spreading procurement across multiple vendors to avoid depending on a single supplier. Diversifying your suppliers is a preventative measure and helps you:

- Minimize disruptions to your supply chain.

- Maintain production schedules.

- Make products available on demand.

4. Work on customer service

Your sales numbers depend largely on how you treat prospects and customers. Beyond getting the product and pricing right, selling is also about providing customers with an experience that makes your company stand out from your competitors and leaves people wanting more business from you.

You can improve your customer service by:

- Acknowledging customer needs.

- Providing personalized support.

- Making customer interactions effortless and enjoyable.

5. Record and analyze all lost sales

A record of all the sales opportunities you’ve lost can be a goldmine of insights into what your business or firm needs to modify. With adequate analysis of this data, you can identify the reasons for those lost opportunities and chart a new course.

6. Leverage technology

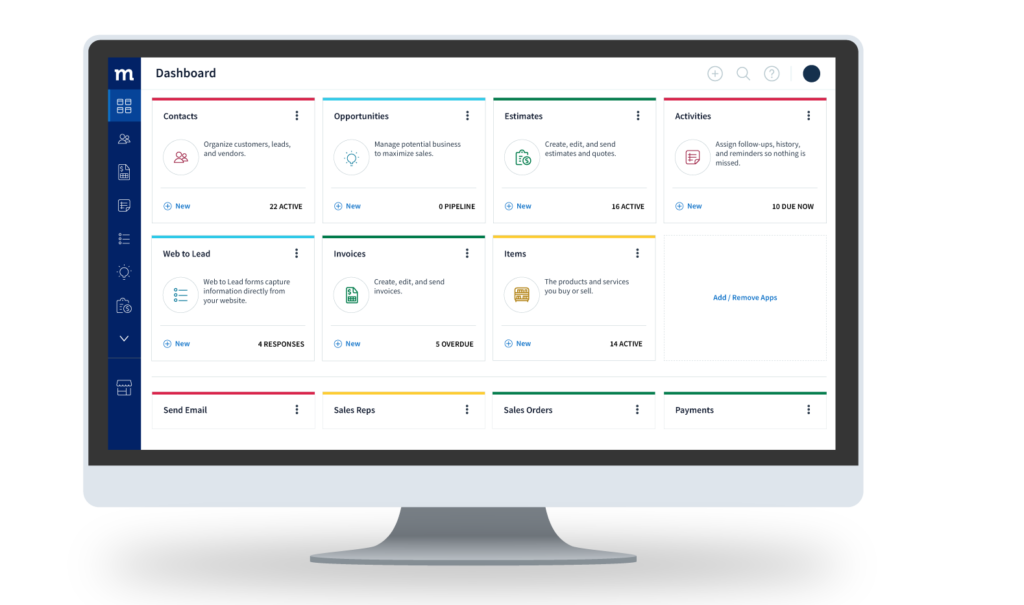

Technology essentially gives businesses superpowers—tap into that power to optimize your sales funnel. If you’re a QuickBooks or Xero user, a CRM software solution like Method can help ensure you don’t miss potential sales due to overlooked or mishandled interactions.

7. Revisit old opportunities

Take another look at lost or stalled sales opportunities to see what went wrong in the past. Analyze previous conversations and reinitiate contact—but this time, focus on helping the customer instead of making a sale. Some cases may have just resulted from bad timing, which you can try to get right as you re-engage.

Minimize lost opportunities with Method

Method CRM helps prevent lost sales opportunities by automating and organizing your sales workflow, ensuring that no potential deal slips through the cracks. Here are just a few of the features that make it happen:

- Automated lead management: Automatically capture and track leads from Gmail or Outlook.

- Sales pipeline tracking: Assign probability percentages to each sales stage, helping prioritize high-potential deals and focus efforts on closing them.

- Workflow automation: Automate follow-ups, reminders, and task assignments to ensure timely engagement with prospects and prevent missed opportunities.

- QuickBooks integration: Sync customer data, invoices, and estimates seamlessly to avoid errors and delays in your sales process.

- Customization: With help from dedicated experts, tailor your CRM to your specific business needs and align things perfectly with your sales workflow.

Using tools like Method helps you transform potential deals into successful transactions, ensuring that all your opportunities are recognized, seized, and converted into sales.

Ready to see for yourself how Method prevents lost sales opportunities? Try it free for 14 days.

Lost sales opportunity FAQs

What does closed-lost mean?

“Closed-Lost” refers to a sales opportunity that has reached its conclusion, resulting in the customer choosing not to proceed with the purchase. This outcome signifies that the sales process has ended, and the deal will not be revived or revisited. That said, you can always follow up on closed-lost deals down the line to try to win them over.

What’s the difference between a lost deal and a lost sales opportunity?

A lost deal refers to a specific sales transaction that failed to close, resulting in zero revenue generation. This typically occurs when:

- A customer chooses a competitor’s offer.

- Negotiations break down.

- Pricing or terms aren’t agreed upon.

- The deal falls through due to external factors such as funding issues.

Lost sales opportunities often result from process issues and encompass potential sales that have slipped away due to various factors, including:

- Unfollowed leads.

- Unqualified leads.

- Misaligned sales strategies.

- Poor customer engagement.

- Missed follow-ups.

Is a lost sales opportunity gone for good?

A lost sales opportunity isn’t always gone for good. While the initial opportunity may have slipped away, businesses can potentially revive or recapture the sale through strategic follow-up, nurturing, and re-engagement.